Wizz Air Holdings Plc, operator of Europe’s seventh largest airline, has released results for the third quarter of fiscal year 2026 on 29 January 2026. The period covered October to December 2025.

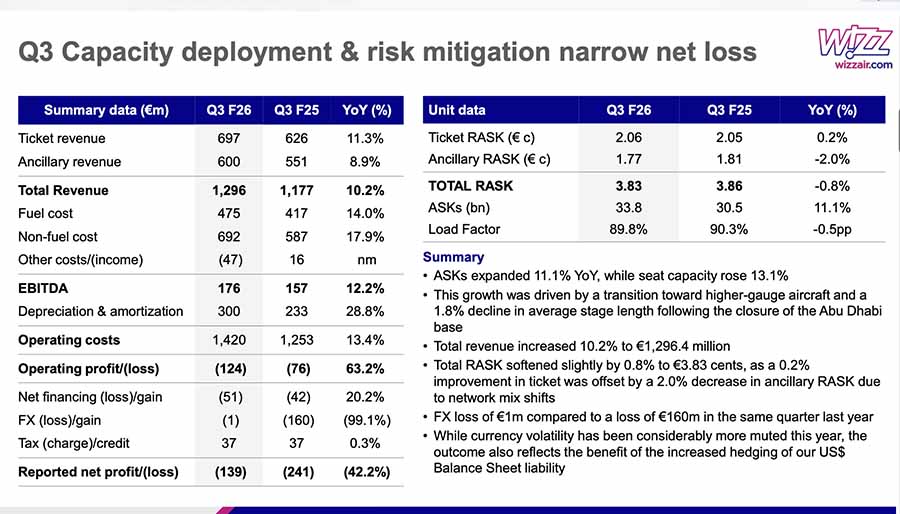

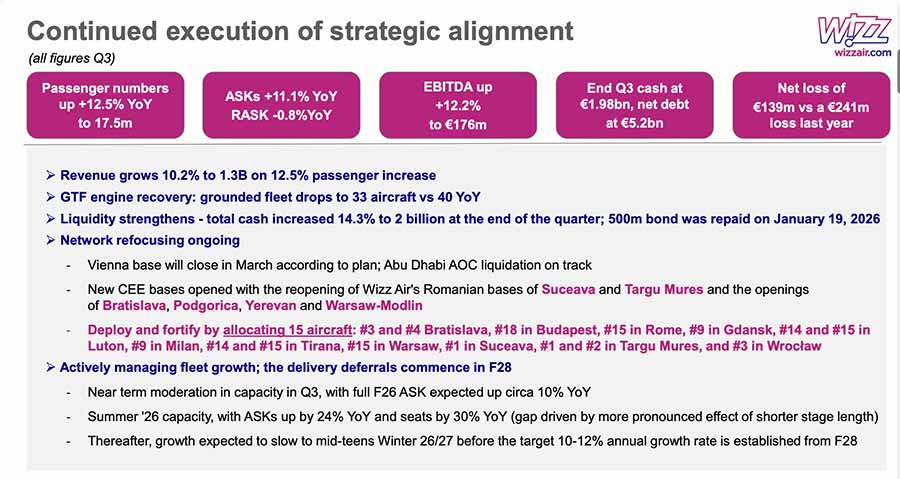

Revenue reached €1.30bn compared to €1.18bn in the prior year. Passenger ticket revenue amounted to 696.9m compared to €627.3m. Ancillary revenue totalled €599.1m compared to €549.7m. Cost per passenger was €81.31. Wizz carried 17,464,295 in the quarter.

Operating loss stood at €123.9m compared to €75.9m. Loss before income tax amounted to €175.9m compared to €277.6m.

Net loss is attributable to owners of the parent reached €140.8m compared to €237.9m. Passengers carried numbered 17.5m compared to 15.5m. Available seat kilometres totalled 33,849m compared to 30,480m. Load factor registered 89.8pc compared to 90.3pc.

The company expects available seat kilometre capacity growth of around 10pc for the full year. Unit revenue forecast remains flat for the year. Forward bookings are tracking ahead of the prior year. Analysts are projecting an operating loss of €137.95m for the quarter.

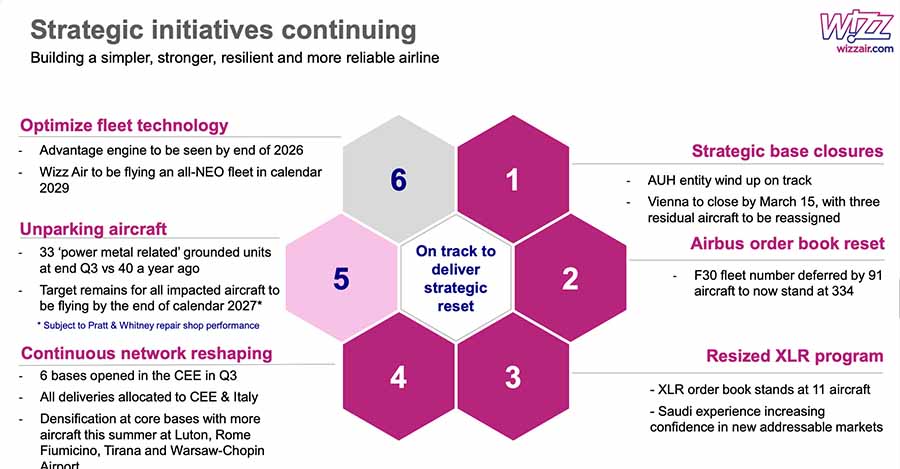

The company focuses on network expansion in Central and Eastern Europe, Italy, and London. Pratt & Whitney engine disruptions continue to affect operations.

Wizz Air operates a fleet of 259 Airbus A320 and A321 aircraft. As of 31 December 2025, Wizz Air had 33 aircraft grounded due to GTF engine-related inspections

József Váradi, Wizz Air Chief Executive Officer shared: “We continue to execute the commercial strategy we outlined earlier this fiscal year, focusing on fortifying our key bases and concentrating our efforts on network design across Central & Eastern Europe, Italy and London. This helps us to better manage RASK while allowing us to concentrate on the ex-fuel cost lines that are most heavily impacted by the Pratt & Whitney GTF engine-related disruptions affecting the Company for the past two years.

Our operations have delivered strong reliability and punctuality, continuing the trend from the summer. Commercially, we continued to invest into all our existing markets, putting on sale new flights and announcing further aircraft allocations for next summer. During the period our fleet size surpassed 250 aircraft, we continue to increase the share of NEO aircraft (nearly 75pc) in our fleet, as well as seat density (now, an average of 230 seats per aircraft). We are steadily recovering from the engine related aircraft grounding and in the next fiscal year we are targeting to have an average of 20-25 aircraft on the ground due to powered metal issues.” F26 OUTLOOK “The ASK capacity for full F26 is expected to grow around 10pc over the previous year.

Based on a forward booking curve the bookings are currently ahead of last year. The expectation is that load factor for F26 finishes north of 91pc, similar as last year. We see similar unit revenue trends we have seen at the start of last quarter (Q3) and we are forecasting flat YoY unit revenue for F26. Total unit costs for full F26 may see modest inflation vs last year as we forecast increased navigation costs from higher Eurocontrol rates, maintenance costs due to inflationary pressures, partly reflecting the uncertainty around Pratt & Whitney’s engine redeliveries from shop visits and higher depreciation costs related to the retirement schedule of the A320ceo family.”

See report here and presentations here.